Massive Federal Reserve still growing amidst inflation

By Bill Bergman. March 10, 2022

In banking and insurance, rapid growth can be a red flag. It’s easy to grow in these industries, at least in the short run, by underpricing services and assuming higher risk.

Today, the Federal Reserve Board issued its weekly “H.4.1” statistical release. This report, titled “Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks,” contains a consolidated balance sheet for the 12 Federal Reserve Banks.

Reserve Bank assets totaled $8.9 trillion in the latest week, up from a month earlier, which in turn was higher than the month before that. The Federal Reserve continues to grow, not shrink, even as inflation has accelerated in recent months.

At $8.9 trillion, the Fed’s total assets were nearly 20% higher than a year ago – and more than twice as high as a few short years ago.

The Fed’s balance sheet is now 10 times as large as it was back in 2006, before its response to the financial and economic crisis of 2008-2009 – a crisis in important part of the Fed’s own making.

There’s no such thing as a free lunch, the saying goes. Is our massive, rapidly growing central bank a source of strength for the government? Even if it is, what’s good for the government isn’t always good for the Average Joe and Jane.

Are our fiscal and monetary oligarchs doubling down on their bets, with citizens in general bearing the downside risk?

Below are many of the hundreds of blog articles I wrote at Truth in Accounting in the decade ended early 2022.

Did Chicago’s finances improve last year?

July 13, 2018

Yes and no, depending on what you mean by “Chicago,” and what you think of the Rule of Law.

The “bottom lines” for Chicago’s income statement and balance sheet both suggested continued deterioration last year, but a closer look presents a mixed picture.

The city’s overall reported financial condition continued to deteriorate, even after especially bad years reported for 2015 and 2016. The city’s reported expenses exceeded fees, grants, and general revenues (taxes), by nearly $1 billion, in line with results in 2012-2014. That loss (in the income statement, called the “Statement of Activities”) was consistent with a continued decline in the net position on the balance sheet (the “Statement of Net Position”).

The nearly $1 billion income statement loss arrived despite reported overall expenses falling almost 20%. The city’s revenues have been catching up to expenses, at least according to these reported numbers, just not enough. Total expenses still run significantly ahead of revenues, despite relatively rapid revenue growth.

Things get interesting when you consider that expectations for sharply higher city contributions to pension plans (and associated tax increases) drove the reported expense decline in 2017, as well as a significant reduction in the net pension liability.

Things get really interesting (and significantly more complicated) when you ask the question why the city’s net position fell further, despite that fact that reported assets rose while reported liabilities declined.

Normally, when assets go up and liabilities go down, the net position improves, right? Not in state and local government land, where the accounting standard setters have recently introduced (a topic for another day, or century) extraordinary new accounts called “Deferred Outflows of Resources” (included near and added to the assets) and “Deferred Inflows of Resources” (included near and added to the liabilities).

Longer story short, significant questions attach to the validity and significance of these ‘deferred’ accounts. Ignoring them, it looks like the city’s finances improved. The city's finances may have improved, but that doesn't necessarily mean that Chicagoans' finances improved, if they are going to be paying significantly higher taxes.

But if recent experience is a guide, the anticipated increases in contributions to employee pension plans driving the reported pension liability reduction may not come to pass. Five years ago, two of the largest plans (Chicago police and firefighter pensions) were expecting significant increases in contributions from 2013 to 2017. The statutory contribution reported for the police fund in 2017 came about $100 million (20%) below what was projected in 2013 for 2017.

Laws come and go, and the ability and willingness of the government to abide by its own laws can be problematic.

Consider that the City of Chicago’s recently released annual report was not available until July 11, even though state law requires it to be published by June 30. And the date on the letter of transmittal (addressed in part to the citizens of the City of Chicago) was June 29, the day before the legal deadline.

Skimming the news—about states that are ‘skimming’

July 24, 2018

Some government funds flow into a variety of tributaries.

Our daily Morning Call e-newsletter summary included two articles today that identified subsets of the 50 states engaged in interesting - and curious - financial practices.

An article in the Daily Signal by Fred Lucas (“Trump Administration Takes on Unions Over ‘Skimming’ Medicaid Payments”) discusses how 11 states deduct a portion of money paid to Medicaid service providers, and send that money to public-sector unions.

And in an article for Forbes (“Yes, Let’s Expand Social Security – To Public Sector Employees”), Elizabeth Bauer identified 15 states where public-sector employees aren’t covered by Social Security.

The issues in these articles deserve more thorough analysis and discussion. But for now, let’s take a look at those first 11 states, and see how they compare to the rest of the 50 states on a number of economic, demographic, and financial characteristics. We can do that using Truth in Accounting’s State Data Lab website.

The 11 states that “skim” Medicaid include California, Connecticut, Illinois, Maryland, Massachusetts, Minnesota, Missouri, New Jersey, Oregon, Vermont, and Washington.

Skimming this list of “skimming” states, it looks like many of them are near the bottom of the barrel in our ranking of the 50 states based on their financial condition. That’s certainly the result—the average Taxpayer Burden™ we calculate for these states comes to $27,000, more than four times as high as the average for the other 37 continental states..

Which comes first, the chicken or the egg? Are states in bad shape because they take money from programs for poor people and give it to their public-sector unions? Are states that take money from services for poor people to give it to public-sector unions doing so because they are in bad financial shape? What else is going on beneath the surface?

We aren’t going to answer those kinds of questions here, but consider some other interesting relationships:

· As one might expect, public sector union representation is higher in the skimming states. The average share of the public-sector workforce covered by collective bargaining agreements is about 50 percent in those 11 states, compared to an average 30 percent in the other states.

· The share of Medicaid enrollment in total population is not significantly different between the skimming and non-skimming states. However, the share of doctors accepting new Medicaid patients (a measure of Medicaid service quality for poor people) was running significantly lower in the skimming’ states a few years ago, while the Medicaid-to-Medicare fee index was running significantly higher in the skimming states than the other states.

· Governments often contract with nonprofits to provide social services for poor people. In recent years, growing financial stress in some governments has been reflected in late and/or lower payments not only to doctors in the Medicaid program, but for nonprofit organizations that provide these services. In a recent survey, the share of nonprofits reporting significant problems with late payments on these contracts ran significantly higher in the skimming states than the other states.

· The states that skim Medicaid payments rank significantly lower than the other states on citizen trust in state government, looking at a recent nationwide public opinion poll.

The Forbes article was not, strictly speaking, about public-sector unions. But the article citation for the list of the 15 states was linked to the National Education Association, a teachers’ union described by Wikipedia as “the largest labor union and professional interest group in the United States.”

The NEA introduced its list of 15 states as “states in which public employees are not covered by Social Security,” and they included Alaska, California, Colorado, Connecticut, Georgia, Illinois, Kentucky, Louisiana, Maine, Massachusetts, Missouri, Nevada, Ohio, Rhode Island, and Texas.

We’ll take a closer look at these 15 states, and broader questions relating to both articles, another day.

Addendum: This article started with the sentence "Some government funds flow into a variety of tributaries." I just looked up "tributary" in the dictionary, to make sure I had the right metaphor. The definition includes "1) a river or stream flowing into a larger river or lake. 2) historical -- a person or state that pays tribute to another state or ruler."

Is Chicago a government version of Enron?

July 31, 2018

The Enron blow-up in 2001 provided lessons to be wary of off-balance-sheet debts. Today, City of Chicago provides some eerie similarities.

Chicago has accumulated rapidly growing debt, including bank loans and bonded debt, as well as obligations in other places. For many years, some of the largest debts (pension and health care benefits for retired employees) were left off the city’s balance sheet. That has changed in recent years as governmental accounting standards have finally required them to be included.

But the City of Chicago does not include a few interesting things on its financial statements. These include the Chicago Public Schools (CPS), the Chicago Housing Authority, the Chicago Transit Authority, and the Chicago Park District.

CPS paints its own dire financial picture, but Chicago does not blend the large negative financial position for CPS in the city’s own balance sheet.

How does it justify this? Chicago’s latest annual financial report notes “The financial reporting entity consists of the City and its component units, which are legally separate organizations for which the City is financially accountable. … The City’s officials are responsible for appointing a voting majority of the members of the boards of other organizations, but the City’s accountability for these organizations does not extend beyond making appointments and no financial accountability or fiscal dependency exists between the City and these organizations.”

Back in the late 1990s, Enron was providing a seemingly smashing success story. Enron’s stock price ballooned from about $10 per share in the early 1990s to a high of $90, before crashing to Earth (and $0) in 2001. Enron’s reported financials were masking a complex Ponzi scheme, one that relied on deceptive reporting to keep a spigot of fresh money coming in the door—until it didn’t.

The complex deals in Enron’s tool chest were in an area called “structured finance.” A respected textbook on the subject by Frank Fabozzi, Henry Davis and Moorad Choudhry called out some of Enron’s practices by saying “Liabilities that truly have no recourse to a company’s shareholders can justly be treated as off-balance-sheet. Enron appears to have violated this principle …”

In 2003, Bethany McLean and Peter Elkind told the Enron story in a best-selling book (which turned into a successful movie) titled “The Smartest Guys in the Room.” Summarizing some of the skullduggery, the authors stated “All the structured-finance deals Fastow and his team cooked up were meant to accomplish a fairly simple set of goals: keep fresh debt off the books, camouflage existing debt, book earnings, or create operating cash flow. At their absolute essence, the deals were intended to allow Enron to borrow money – billions upon billions of dollars that it needed to keep itself going – while disguising the true extent of its indebtedness.”

Granted, Enron was a pretty unique case, and Chicago is joined by other cities in not consolidating public school systems in its own books. And Chicago funding includes a significant slice of tax money, which arrives not exactly freely but through a rule of law (and force). But the similarities are a little disturbing.

In this light, consider the City of Chicago’s current and ongoing claim that “no financial accountability or fiscal dependency exists between the City and these organizations” – including the Chicago Public Schools.

The following quotes are lifted directly from the latest proposed budget for the Chicago Public Schools. Do you think any fiscal dependency exists?

· “The FY2019 budget also includes nearly $1 billion in capital spending — the largest single-year investment since the Mayor of the City of Chicago became accountable for the performance of CPS.”

· “CPS has received more than $1.3 billion in TIF funds for capital investments in schools throughout the city over the past decade.”

· “On top of capital expenditures on schools, Mayor Emanuel is also committed to declaring a surplus of TIF funds each year.”

· “ … “All other local” revenue includes the pension payment made by the City of Chicago on behalf of CPS employees to the Municipal Employees’ Annuity and Benefit Fund of Chicago (MEABF), and is estimated to be $52 million in FY2019. It is recorded as revenue as required by the Governmental Accounting Standards Board (GASB).”

· “FY2019 local contributions to capital projects are expected to be $32.5 million. This includes $18 million in TIF-related project reimbursements and $14.5 million from other local funding sources.”

· “Other Federal Grants …include competitive grants for other specific purposes. Below is a brief description of major grants under this category … CPS Head Start programs are funded through the City of Chicago. CPS anticipates receiving $36 million for the FY2019 Head Start program to serve all eligible enrolled students.”

· “The Law Department provides legal services to the Chicago Board of Education, schools, and the departments and divisions of the Chicago Public Schools. … MAJOR ACCOMPLISHMENTS … Drafted, negotiated, and/or provided advice concerning more than 1,000 contract matters, including: (a) a $1 million grant agreement from the City of Chicago Department of Family Support and Services to assist CPS in curricula development, instructional support, and computer science toolkits to help high schools develop implementation plans for the new Computer Science graduation requirement …”

· “Debt Management … CPS funds its Capital Improvement Program largely through the issuance of bonds. … As of June 30, 2018, the Board of Education has approximately $8.2 billion of outstanding long-term debt and $600 million of outstanding short-term debt. … CPS issues bonds backed by the full faith and credit of the Board, otherwise known as General Obligation (GO) Bonds. These GO bonds are paid for from all legally available revenues of the Board. … The first revenue source that is supporting CPS bonds is one of the following: EBF, Personal Property Replacement Taxes (PPRT), revenues derived from intergovernmental agreements with the City of Chicago, property taxes, and federal interest subsidies. The majority of CPS bonds are backed by EBF. … Additionally, $113 million in debt service will be paid by revenue resulting from Intergovernmental Agreements with the City of Chicago.”

· “By law, the City of Chicago has been contributing to the Municipal Employees’ Annuity and Benefit Fund of Chicago on behalf of the Board’s educational support personnel (ESP).”

· “Inter-government Agreement (1997 IGA) with City of Chicago - October 1, 1997: … The 1997 IGA represents a unique financing arrangement between the city of Chicago and the Chicago Public Schools to pay for the construction of new schools, school building additions, and renovation of existing schools and equipment. Per the agreement, the city will help the Board to finance its Capital Improvement Program by providing it with funds to be used to pay debt service on bonds issued by the Board for such purpose. The amount to be provided by the city will be derived from the proceeds of ad valorem taxes levied in future years by the city on all taxable property.”

Massachusetts town police force quits en masse

August 1, 2018

NBC News reports that the entire police force (4 officers) of Blandford, Mass., (population 1,253) quit yesterday. The officers issued a statement citing concerns about how the town is asking them to patrol in cars without air conditioning, properly working brakes, snow tires, or four-wheel drive.

One has to wonder whether city financial problems are part of the equation, so I checked out the town’s website and found that the list of annual financial statements ends at 2011.

When I called town administrator’s office to inquire more about the recent financial reports, I was told the town simply hasn’t published them since 2011. This year, however, Blandford has retained outside accountants, and the town official expressed confidence that they can produce audited results again.

While the town website does have a version of a financial report for 2018 up there, it’s a video that starts with an interesting choice in background music — Getting Better by The Beatles.

Chicago’s new budget document shows city finances ‘getting better’

August 1, 2018

Chicago’s latest Annual Financial Analysis (released yesterday) suggests that city finances are still deteriorating.

The document's base outlook projects what the city calls a “structural budget deficit” (an excess of forecast expenditures over revenue) of nearly $100 million in 2019. These fiscal forecasts have been improving in recent years, as stressed by the Mayor, at least in the sense that the projected deficit has been declining. But in the end, a deficit is still a deficit.

It is worth noting that these annual projections include not only the next budget year, but the following year as well. Last year, the city projected a base outlook deficit of $212.7 million for 2019. While this year’s expectation is for a deficit of about $100 million in 2019, the projections for future years’ deficits continue to climb (i.e., negative numbers getting bigger).

It is also worth stressing, every year, that these budget reports are not actual results, but projections. There are words and there are deeds, and the results of the deeds arrive in the audited annual financial statements. Those statements are based on more reliable accrual-based accounting standards, and have shown expenses running ahead of revenues in recent years, leading to significant declines in Chicago’s net financial position even as the city maintains that it balances its budget as required by state law.

We’ll be taking a deeper dive into Chicago’s latest Annual Financial Analysis soon, but it is worth starting with the very first substantive section in the report: the “Disclaimer and Advice to Readers.” The city began including a disclaimer in the budget document in the Annual Financial Analysis for 2016; previously, the first section of the report was the “Letter from the Mayor.”

A new paragraph in the disclaimer this year reads as follows:

“Readers are cautioned not to place undue reliance on the prospective financial information. Neither the City, the City’s independent auditors, nor any other independent accountants have compiled, examined, or performed any procedures with respect to the prospective financial information contained herein, nor have they expressed any opinion or any other form of assurance on such information or its achievability, and assume no responsibility for, and disclaim any association with, the prospective financial information.”

In other words, don’t pay too much attention to this.

Chicago’s pension obligation bonds – swapping one credit card for another?

August 16, 2018

The City of Chicago is reportedly considering a pension obligation bond offering. The city could issue $10 billion in bonds, and use the proceeds to fund its pension plans. A decision could come as soon as Friday.

The idea has been criticized from several quarters. One critic called it “just swapping one credit card for another.”

It could be significantly worse than that. Here’s a simple scenario illustrating what can happen with pension obligation bonds, depending on how they are structured.

Let’s assume a simple city that has two main parts – a pension plan for employees, and everything else in city government. Assume the rest of the city’s government has $500 in assets, no debt, and therefore a net position (assets less liabilities) of $500. The city’s pension plan has assets of $500, but a liability (to pensioners) of $1,500, and therefore a negative net position ($1,000).

Consolidating the rest of the city with its pension plan, you have an organization with $1,000 in assets, $1,500 in liabilities, and a negative net position of $500.

Now, let’s ‘fix’ that pension plan. We borrow $1,000, selling a pension obligation bond. We take the proceeds, and put them into the pension plan.

Poof, problem solved? The pension plan’s funded ratio goes from 33 percent (500/1500) to 100 percent (1500/1500).

But what about the rest of the city, and the consolidated balance sheet?

The consolidated balance sheet a) gets bigger, and b) gets more risky. Total assets go from $1,000 to $2,000, as assets managed for the plan go up. Liabilities go up by the amount of the bond offering, rising from $1,500 to $2,500. The net position ($2,000-$2,500) is unchanged (negative $500), consistent with a neutral ‘swapping one credit card for another’ interpretation.

But consider a 20 percent decline in the value of the investments in the pension plan, and what happens to the consolidated net position before and after the pension obligation bond.

Without the pension obligation bond, assets in the pension plan fall $100, leaving a net position for the consolidated enterprise of $900 less $1,500, or negative $600 (down from a negative $500).

Adding the pension bond, and assuming the same 20 percent decline in the value of invested assets in the pension plan, the pension plan assets fall from $1,500 to $1,200, leaving the consolidated enterprise with $1,700 in assets, $2,500 in liabilities, and a negative net position of $800 – a bigger hit (from a negative $500 to negative $800) than the impact that would have arrived without the pension bond.

How about the rest of the city? Before the pension bond, the rest of the city had $500 and no debt. With the pension obligation bond, the city issues the bond, puts the proceeds in the pension plan. Total assets stay the same ($500), while total liabilities rise (from $0 to $1,000), turning a positive net position of $500 into a negative net position (negative $500).

But the pensioners feel better, given that fund assets are higher and more unambiguously in the pension plan.

Are states sitting on piles of cash, at the expense of their cities?

August 21, 2018

Last week, Timothy Williams wrote an article in the New York Times examining a debate in some states over what to do with rising ‘surpluses,’ and whether they should be saved in rainy-funds or redistributed to cities with pressing cash-flow requirements. Among other things, he penned “Still, the combination of a surplus and fresh revenue means that states that had endured years of involuntary frugality are virtually swimming in cash.”

The rhetoric over surpluses, and public perception, could benefit from a refresher course on the differences between cash-flow accounting and accrual accounting. They could also benefit from reminders about the differences between income statements and cash flow statements, on the one hand, and balance sheets, on the other hand.

Consider a family running a current cash flow surplus, but it has two daughters about to head off to college for the fall semester. They just took out large student loans to help the girls get to their launch pads. Should this family go out to dinner every night this week, and celebrate their departure?

That’s an unfair comparison, of course. Cities looking at states ‘swimming in cash’ assert they have pressing requirements for their citizens.

But maybe some of those states and their city children need to pay more attention to the longer-term consequences of past and current financial practices, buckle their belts, and get more efficient.

Another distinction between the family example and the state/city comparison has to do with mobility. What if that family is in a state asserting ‘balanced budgets,’ and ‘current surpluses,’ but has accumulated massive long-term debts that have to paid down the road?

Families can move. States and cities can’t.

What is the PBGC, and why should you care about it?

August 23, 2018

Concerns have been growing over the financial health of the federal government’s Pension Benefit Guaranty Corporation (PBGC). This entity backs up “private sector” pension plans, but failures to adequately fund the plans backed by the backstop, as well as the backstop itself, now threaten the pensions of millions of workers and retirees.

Those threatened now include taxpayers, given the PBGC is a federal government entity.

Late last year, an Ohio senator introduced the “Butch Lewis Act of 2017.” Among other elements, the proposed law would create a new Pension Rehabilitation Trust Fund authorized to make loans to troubled pension plans.

Earlier this year, Congress created a new joint House/Senate Committee dedicated to the issues underlying multiemployer pension plans and the PBGC. The Joint Select Committee on Solvency of Multiemployer Pension Plans is chaired by Sen. Orrin Hatch (R-Utah) and Rep. Sherrod Brown (D-Ohio). Back in April, this committee issued a request for comments on the Butch Lewis Act and related issues.

But in an ominous sign, the request for input identified who the Committee was seeking input from. The statement said they were seeking out the views of ‘stakeholders,’ with Rep. Brown identifying ‘workers, retirees, and businesses.’

He didn’t identify taxpayers, or citizens, as stakeholders.

You can participate anyway, though. Comments are due mid-September.

Should ‘state stress tests’ stress pensions, or states?

August 24, 2018

In 2010, on the heels of the worst financial crisis since the Great Depression, Congress enacted the Dodd-Frank Act. Section 165 of this 849-page law directed the Federal Reserve Board of Governors to develop and apply “stress tests” to large bank holding companies and other financial institutions.

Stress tests are hypothetical accounting and financial modelling exercises that attempt to estimate the impact of adverse economic and financial market developments on the soundness of financial firms. The conduct and implications of these tests have had mixed reviews. Some proponents contend stress tests improve the resilience and stability of the financial system. Critics question whether those tests have been sufficiently stressful, and some even question their utility at all.

Anat Admati, a finance professor at Stanford University and an advocate for significantly higher capital requirements in banking, has called the tests a “charade.” Kevin Dowd wrote an analysis for the Cato Institute titled “Math Gone Mad,” which argues the tests in practice actually “create the potential for a new systemic crisis.”

Banks aren’t the only stressful financial institutions around. The concept of stress testing has spread. The Pew Charitable Trusts, a widely cited authority on pension plans, has been banging the drums especially hard this year. Pew, together with Harvard’s Kennedy School of Government, has developed a set of modelling tools for states to apply in stress tests for their pension plans. A growing number of states has begun to require these tests.

It sure sounds good, on the surface. Why not subject these risky pension plans to rigorous scrutiny? Isn’t that a responsible thing to do?

In practice, however, stress tests have the potential to bias risk allocation in ways preferred by well-organized special interest groups, at the expense of citizens, taxpayers, and the Average Joe and Jane.

Take a peek at a lengthy paper Pew issued a few months ago. Titled “Assessing the Risk of Fiscal Distress for Public Pensions: State Stress Test Analysis,” Greg Mennis, Susan Banta and David Draine reported on the results of applying their tests to public pension plans in 10 states, and recommended that stress tests become a standard reporting practice for all public-sector retirement systems.

Consider who they stressed, however. The title may have been subtitled “State Stress Test Analysis,” but states weren’t the organizations being stressed. The pensions were the object of the analysis.

Improving the stability of pension finances may reduce risks for state government operations and taxpayers. However, focusing on pensions and reducing plan risk can also come at the expense of, and pose higher risk to, other government operations, as well as taxpayers and citizens.

In their May 2018 paper, for example, Mennis, Banta and Draine praise Wisconsin and North Carolina for demonstrating “how strong funding policies can help to ensure that public pension systems are sustainable and secure.” Wisconsin and North Carolina certainly rank high on their pension funding status, among the 10 states covered by Pew as well as nationally. However, in our holistic analysis of state financial conditions, Wisconsin and North Carolina’s overall financial position don’t rank nearly as high as might be expected given the pension funding because bond borrowing debt runs relatively high in those states.

This can illustrate how a state might strategically work harder to improve its performance in pension stress tests, but at the expense of the general public. Consider what happens when a hypothetical state issues a bond, a bond so large that it leads its funded ratio to rise to 100 percent. The risk to the pension plan has certainly gone down, but the risk for the rest of the state government as a whole has increased.

Chicago is now considering a massive new bond offering designed to fund its woefully underfunded pension obligations. City leaders are reportedly briefing city aldermen ‘behind closed doors.’ The bond offering would certainly improve Chicago pension plans’ odds of passing stress tests. But it would also increase the size and risk of the city’s overall balance sheet.

Stress tests can be abused. If they can be applied honestly, they should focus on the right entity, not a special, favored subset of government.

Looking at Illinois and Indiana migration trends with State Data Lab

August 28, 2018

Truth in Accounting’s State Data Lab website includes a wide variety of demographic, economic and government financial information for all 50 states and 75 of the largest cities in the US.

“Where should you move?” is our theme of the week this week. State Data Lab can help inform your decision, if you are thinking along these lines.

You can also use State Data Lab to look at migration trends, even if you aren’t thinking about moving. We have a variety of population and related migration data in there.

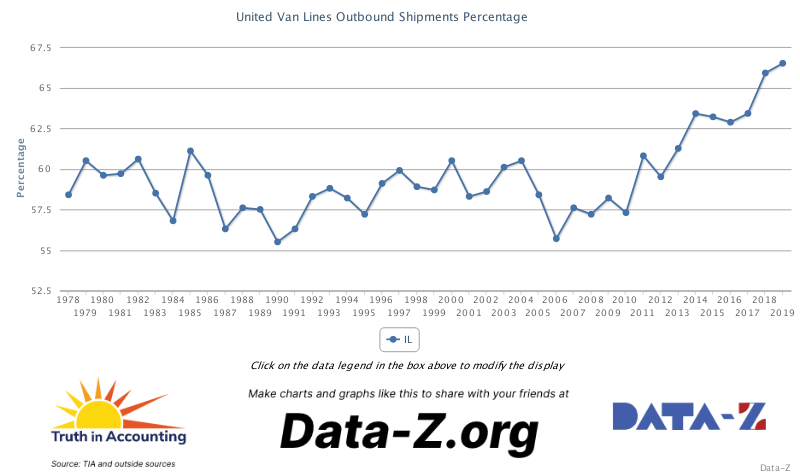

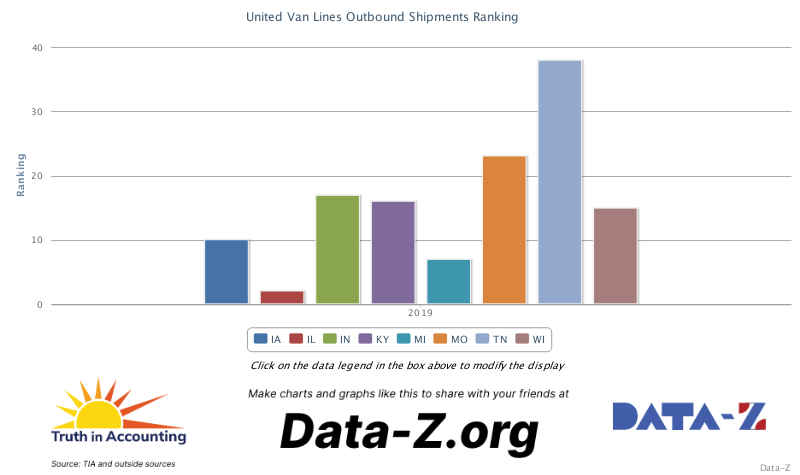

For example, United Van lines, one of the largest interstate moving companies in the US, has published an annual migration study each year since 1978. We include the results from that study for all 48 continental states since 1978.

Let’s take a peek at Illinois and Indiana results on this study since 2005.

State Data Lab is really easy to use. Just go to the website (www.statedatalab.org). Then:

1. At the top of the front page, hover over “CHARTS.”

2. Click on “CREATE YOUR OWN CHART” in the dropdown box.

3. Click on Illinois and Indiana to choose those states, in Step 1. Then ...

4. Head down to the “DEMOGRAPHIC” section. The first subsection in there is called “Population.” Near the bottom of that section, click on “United Van Lines Outbound Shipments Percentage.”

5. Move down further, below all the data variables, to Step 3, “SELECT AVAILABLE YEARS.” Click on all the years 2005-2017 indvidually.

6. Then, below that, click on “GENERATE CHART.” A column chart will be generated. Change it to a line chart in the dropdown box. Here’s what you should see.

7. You can easily share this chart with others. One way is to generate a URL. Below the chart, in “SHARE YOUR CHART,” click on “Share Your Chart.” That will generate a unique URL that you can copy and send to others and they can click on it and get their own chart. Or, you can save the chart as a picture file, and send it that way.

It isn’t a pretty picture, for Illinois at least. Illinois is leading the nation in outbound moves in recent years. Consider the difference between Illinois and Indiana, and note that it isn’t the hardest comparison for Illinois, either – Indiana has had positive net outmigration in recent years.

Don’t worry about pension liabilities – the stock market went up a lot two years ago

August 30, 2018

Balance sheets and income statements have different time perspectives. Income statements tell a story about performance over a period of time, while balance sheets, in theory, tell a story about financial position at a point in time.

Income statements and balance sheets each lead to a bottom line that should inform the residual claim the enterprise is accountable to. On the income statement, revenue less expenses leave what is left over for the ultimate claim on the enterprise. On the balance sheet, assets less liabilities leave a net position.

For state and local governments, accounting standards have developed the Statement of Activities (the income statement) and the Statement of Net Position (the balance sheet). For decades, however, the Statement of Net Position excluded retirement benefit obligations from the debts, which have blossomed into the largest liabilities for many state and local governments.

In fiscal 2015, governments began including these debts, as they were finally required to do so. But the face of the balance sheet did not include investment assets supporting retirement plans, or the full liability estimated for those assets to support. Instead, they included the net pension liability – the full liability less the invested assets. Given that the vast majority of retirement plans operate with less assets than measured liability, this led to a large increase in reported debt, and significant deterioration in the net position.

But the way in which governments include this net liability on the balance sheet (the Statement of Net Position) has some very curious features. One of the strangest can be illustrated with a statement by Moody’s Investor Service a few days ago.

In a press release titled “Unfunded US state pension liabilities surge in fiscal 2017 due to poor investment returns,” Moody’s first paragraph reads as follows:

“The majority of US states experienced a sharp increase in their adjusted net pension liabilities (ANPL) in fiscal year 2017, owing to poor investment returns in fiscal 2016, Moody's Investors Service says in a new report. However, favorable investment returns in fiscal 2017 and 2018 are expected to lead to a decline in pension liabilities for the next two fiscal years.”

Fiscal 2016 ended, for most states, on June 30 2016. How can that lead to deterioration in net position for year-end fiscal 2017, you ask?

In turn, consider how Moody’s can accurately 'forecast' pension liabilities declining for the next two fiscal years, given that investment returns were so favorable over the past two years ended June 30, 2018.

So much for that “point in time” perspective for balance sheets.

New Hampshire’s “Economic Advantage” index - what does it tell Illinois?

August 30, 2018

Dave Lemery at Watchdog.org recently wrote an article titled, “New Index Seeks to Quantify ‘New Hampshire Advantage’ Over Neighboring States.” The article tells the story of a new index developed by the Granite Institute, a right-leaning public policy think tank . The index is used to compare New Hampshire to its neighbors on economic growth and factors that may promote (or impede) growth. The index appeared to confirm anecdotal references to the ‘New Hampshire Advantage,’ at least relative to neighboring states.

After reading the first two paragraphs, I stopped reading and tried to develop my own index, and to see how it performs compared to the index developed by the Granite Institute. It’s pretty easy to do, at least in quick and dirty fashion, with the tools available on our State Data Lab website.

Since 2003, New Hampshire’s GDP growth has been in the middle of the pack when compared to its neighbors. However, looking at New Hampshire and how it ranks on factors I selected as indicators that can matter for economic growth, New Hampshire indeed ranks highest among its neighbors.

The factors I selected (all of which can be found on State Data Lab) are Forbes’ Best States for Business rankings, the Cato Economic Freedom rankings, rankings on trust in state government according to the most recent Gallup poll, rankings for lawyers per capita (a proxy for regulation), and Truth in Accounting’s Taxpayer Burden rankings.

Collectively, these five indicators do a good job of explaining economic growth differences across the 50 states.

Looking at New Hampshire and its neighbors, here is the average rank for these five factors (the lower the number, the higher the ranking).

New Hampshire ranked the highest compared to its neighbors.

After putting this together, I went back and read the rest of the article. The Granite Institute’s index, which was developed by J. Scott Moody, also relies on five economic metrics, but different ones. They include the size of the private sector in the overall economy, taxes on individuals, taxes on consumption, taxes on businesses, and taxes on wealth.

It is useful to consider our Taxpayer Burden measure compared to current taxes of the types relied on by the Granite Index. “You can pay me now, or pay me later,” the saying goes. States can fund themselves with current taxes as well as accumulating debt, and the latter poses consequences for future taxpayers that can undermine economic growth.

But it is interesting that we came to similar conclusions, after taking different, independent routes. This analysis tends to support the Granite Institute’s conclusions.

Our State Data Lab facility can be used for analyses like this for any region you want.

For example, let’s do the same thing we did for New Hampshire and its neighbors to Illinois and its neighbors. In short, you end up with a chart like this:

Again, bigger isn’t better on this number. Illinois ranks the lowest, compared to its neighbors.

How will Libertarian party candidates fare at the polls in November?

September 7, 2018

We include the Democratic, Republican, and Libertarian party share of the popular vote in Presidential election years in our State Data Lab website.

Looking at the last five Presidential election years, here’s the Libertarian share of the popular vote, on average, across the 50 states:

Growing like a weed.

Was 2016 an anomaly, driven by the success (relatively speaking) of the candidate, Gary Johnson? Or is something more fundamental going on?

Should be fun to watch.

Parenthetically, just noting here that looking things over in State Data Lab, states with a higher Libertarian share of popular vote tend to be in better shape financially, looking at Truth in Accounting’s Taxpayer Burden measure.

Should public pension plan assets be managed for pensioners, or taxpayers?

September 20, 2018

Paul Rose is a law professor at The Ohio State University. Over the weekend, he had an article published in the Illinois Law Review titled “Public Wealth Maximization.” Rose makes a groundbreaking case for the fundamental reshaping of fiduciary duties of managers of public pension funds. Historically, they have been directed to pursue the best interests of plan beneficiaries. Rose argues that they should first and foremost be managed for the benefit of the general public – citizens and taxpayers.

As part of his argument, Rose notes that the legal position of pension plan participants behaves more like a senior claim on government, rather than the residual claim for shareholders in corporations, where managers owe a fiduciary duty to the residual claim. While it may seem that pension plan participants fare well when plan assets are invested well, and they fare poorly if plan assets are invested poorly, that just isn’t the case, especially in places like Illinois where defined pension benefits are guaranteed under state law.

So Rose argues that fiduciary duties should flow to the real risk takers – the public.

Consider a market crash. Do pensioners care? Not if their benefits are defined and guaranteed. Citizens and taxpayers are the ones on the hook. They’ve effectively been placed in the stock market, even if they don’t want to be there – just on the downside.

In discussing the implications of his argument, Rose focuses on what they can mean for investment choices, particularly in light of externalities and issues relating to socially-responsible investing. But his argument also has important – and likely good – implications for risk-shifting to taxpayers, and could result in ‘socially responsible’ investment decisions of a different sort, including less risky investment portfolios for public pension plans.

In a world where pension benefits are defined and guaranteed, and plan managers under a duty to care first and foremost about plan participants, there can be incentives to invest in riskier-than-socially-responsible portfolios when citizens and taxpayers bear any downside of risky investments.

In turn, the idea that pension plan assets should be managed with a view to the public as the residual claim supports an argument I am developing that GASB recognized pension liabilities on balance sheets incorrectly. After decades of leaving them off the balance sheet, GASB finally required the net pension liability – the total liability less plan assets – to be included in the debts of governments. One can make a case, and I am developing it, that GASB should have forced the recognition of the total liability as a debt, along with recognizing plan assets among the assets of the sponsoring government.

New “Zombie Index” helps illuminate risks facing taxpayers

October 9, 2018

In the last week we have had a healthy reminder that stock and bond prices can go down as well as up. Granted, a few days does not make a trend. But it always makes sense to consider darker possible scenarios, particularly for many state and local governments whose financial position has deteriorated since 2009 despite a huge apparent recovery in financial markets.

What would happen in the event of a large, sustained downturn in financial markets, perhaps arising with sustained higher long-term interest rates? Which of the United States are potentially at higher risk than others? With Halloween coming up, we’ve decided to revise and update the “Zombie Index” we include in our State Data Lab database.

This index is inspired by the work of Edward Kane, Professor of finance at Boston College. Kane wrote books warning about the developing crisis in the deposit insurance system in the late 1980s. Kane coined the term "zombie bank," referring to banks and thrifts that were effectively insolvent but allowed to remain open via untruthful accounting and regulatory forbearance.

Kane called them "zombies" because they were really dead but allowed to walk among the living, and false accounting delayed loss recognition. Zombies had incentives to take large risks to try, in Kane's words, to "gamble for resurrection" – especially considering moral hazard generated by expectations that taxpayers would get the downside of the gambles. These incentives, in Kane's view, amplified the cost of the savings and loan crisis for taxpayers.

Similar incentives may still exist today, for “too-big-to-fail banks” as well as troubled state and local governments facing huge shortfalls in their pension plans – shortfalls long left outside government balance sheets.

Our Zombie Index is based on five elements related to what Kane viewed as the factors in Zombie-ness. The first is Truth in Accounting's "Taxpayer Burden" (weighted at 25%), the second is the timeliness (or lack thereof) in filing the annual Comprehensive Annual Financial Report (weighted at 25%), the third is the trend in timeliness (weighted at 10%), the fourth is Truth in Accounting's "Transparency Score" (weighted at 25%) and the fifth is the average ratio of accrual expenses to accrual revenue in the last 10 years (a measure of whether governments really 'walk the talk' on balanced budget requirements, weighted at 15%).

States with higher "Zombie Index" scores may be more likely to be taking higher risks in their investments and other areas. The Zombie Index Ranking is from 1-50, with one indicating the highest Zombie Index ranking, and 50 indicating the lowest ranking.

We report the Zombie Index rankings for 2009 to 2014, and for 2017 onward. Beginning in 2015, state and local governments began including previously off-balance-sheet retirement benefit debt on their balance sheet, changing the nature of the "hidden debt" component previously included in our Zombie Index rankings. We substituted the Transparency Score for that component beginning in 2017, and added the trend in timeliness and the rolling 10-year average ratio of accrual expenses to accrual revenue in 2017 as well.

The biggest ‘Zombies?’ New Jersey, Massachusetts, New Mexico, Connecticut, and Illinois. Taxpayers and citizens in those states could benefit from more oversight of risk exposure in investments backing retirement funds. They might also benefit from some form of ‘prompt corrective action’ advocated by Kane and others for supervisors of failing banks – sooner than later.

Some related possible remedies could include Paul Rose's recent recommendations for considering fundamental changes in the fiduciary responsibilities for public pension fund managers, and Ed Kane's ideas about fiduciary duties for managers of “too-big-to-fail banks.”

Quiz of the Day

October 11, 2018

How many words are in the Illinois Municipal Code? These statutes govern municipalities in Illinois.

a) 510

b) 2,645

c) 3,544

d) 587,287

Answer(s): a) The word ‘money’ appears 510 times in the Illinois Municipal Code. b) There are 2,645 words just in the table of contents in the Illinois Municipal Code. c) The word ‘tax’ appears 3,544 times in the Illinois Municipal Code. d) There are 587,287 words total in the Illinois Municipal Code, almost as many as the King James Bible. Copying and pasting the Illinois Municipal Code into a Word document takes some time, depending on your computer. The Word document runs more than 3,000 pages long.

Chicago’s new ‘balanced’ budget – more of the same

October 18, 2018

Chicago Mayor Rahm Emanuel on Wednesday delivered his annual budget speech.

This was his last budget address, given that he didn’t choose to run for re-election. During his speech, Emanuel claimed that Chicago’s fiscal and economic health "is stronger than it has been in many years."

The veracity of this claim may depend on what the word ‘many’ means.

The mayor asked us to think about where the city was seven years ago.

So let’s do that, especially in light of how the city claims that it balances the budget every year "as required by state law."

Here are five things to take away from Emanuel's latest budget proposal.

1. It’s big.

2. It’s bigger than it used to be.

3. It’s “balanced” – again.

4. It’s “interesting”

5. There are “no new taxes.”

It’s big. Chicago’s new proposed budget calls for more than $10 billion in spending next year.

It’s bigger than it used to be. The proposed spending runs about 30 percent more than proposed in 2011 for 2012. This is curious in light of the mayor's claim, prior to his last re-election, to have “balanced the budget” without significant tax increases, by making the city “smaller, smarter, and simpler.”

It’s “balanced” – again. If the people taking care of your organization’s money told you that they were running a balanced budget, would you think your organization’s debt was going up? Wouldn’t a balanced budget at least keep your debt even, or even decline?

That’s not what’s been happening in Chicago. Expenses ran higher than revenue every year from 2011 to 2017.

From 2011 to 2017, the city’s total reported liabilities doubled, largely because the city finally began including pension obligations on its balance sheet a couple years ago. Excluding pensions, however, Chicago’s total reported liabilities still rose significantly from 2011 to 2017, reflecting how the city was running up the credit cards on its residents, even while telling them they were ‘balancing the budget.’

It’s “interesting.” The new budget includes more than $800 million proposed for debt service. This includes interest on bonded debt. Last year, the City of Chicago incurred more than $720 million in interest expense—up more than $200 million from 2011. That's a lot of dough, especially when it's generated by borrowing to fill gaps in “balanced” budgets.

There are “no new taxes.” Writing in Crain’s Chicago Business, Greg Hinz’s summary was headlined “No tax hikes, two big holes in Emanuel’s final budget.” Hinz is careful to qualify that there are no new tax or fee hikes “beyond those that already have been approved.” The city is in the midst of implementing large-scale property tax and other revenue increases, and the ability and willingness of taxpayers to fork over this money will be tested in the years ahead.

The Civic Federation supports the City of Chicago’s proposed budget

November 1, 2018

The Civic Federation released its annual review of Mayor Rahm Emanuel’s proposed budget for the coming fiscal year. The Civic Federation came out in support of the $8.9 billion budget proposal.

In the Chicago Sun-Times, Fran Spielman summarized the Civic Federation’s review as follows:

“Mayor Rahm Emanuel’s feel-good final budget is a “reasonable one-year financial plan” that keeps the city’s hand out of taxpayers’ pockets but “ignores an enormous elephant in the room,” the Civic Federation warned Wednesday.”

One might argue that it isn’t possible to have a reasonable one-year plan if it ignores an enormous elephant in the room. One could also argue that the city isn’t really taking its hand out of taxpayers’ pockets; the hand is still in there, just waiting for more money when it comes down the road.

In its full report, the Civic Federation cited the city’s projected $100 million shortfall in the Corporate Fund, calling it a “budget deficit.” A footnote that follows states “The City of Chicago is required by law to pass a balanced budget so it does not have a budget ‘deficit’ in the same sense that the federal government has a deficit.” The Civic Federation squared this circle by noting that the city ultimately balances the budget by measures introduced in the annual budget ordinance.

Trouble is, the city of Chicago’s expenses have exceeded revenue every year since 2010 by an average of $2 billion a year. How can you “balance a budget” every year, but spend more than you take in every year? Political math and bad accounting rules provide the answer.

Below is a compilation of the Civic Federation’s summary of this annual report from 2003 to 2018. Each year, the group introduces the report with a statement of support or opposition to the budget proposal. The Civic Federation supported the budget proposal in 13 of those 16 years.

Consider the arguments supporting the appraisal issued in 2010 (for FY2011), the last time the Civic Federation opposed the budget proposal, in light of the concerns cited in the Chicago Sun-Times article cited above.

xxxxx

October 31, 2018

The Civic Federation supports the City of Chicago’s proposed $8.9 billion FY2019 budget because it is a reasonable one-year financial plan that does not include any new taxes or fees, makes important public safety investments and funds the increased 2019 pension contribution of $32 million to the police and fire pension funds without a property tax increase.

November 8, 2017

The Civic Federation supports the proposed FY2018 City of Chicago budget of $8.6 billion because it continues to work toward stabilizing the City’s finances, puts its four pension funds on a path toward solvency and works to incorporate short-term capital expenses into the operating budget rather than funding them through borrowing.

November 1, 2016

In a report released today, the Civic Federation announced its support for the City of Chicago’s proposed FY2017 budget of approximately $8.2 billion because it continues to work toward addressing the City’s unfunded pension liabilities and makes significant improvements over past financial practices.

October 14, 2015

The Civic Federation supports the City of Chicago’s proposed $7.8 billion budget and necessary property tax increase as a long overdue action to address the City’s public safety pension funding crisis.

November 3, 2014

The Civic Federation supports the City of Chicago's proposed $7.3 billion budget because it reflects both reasonable structural changes and significant actions toward long-term stability, including the 2014 pension reform law for the City's Municipal and Laborers' pension funds and the continued phase out of the City's retiree health care subsidy.

November 13, 2013

The Civic Federation supports the City of Chicago’s proposed $7.0 billion budget as a reasonable short-term plan that closes approximately two-thirds of a $338.7 million budget gap with structural changes that will continue to reduce the City’s ongoing deficit.

October 31, 2012

The Civic Federation supports the City of Chicago’s FY2013 proposed $6.5 billion budget which reduces the City’s reliance on one-time revenue sources while restructuring City government through better managing personnel expenditures.

November 2, 2011

The Civic Federation supports the proposed FY2012 City of Chicago budget of nearly $6.3 billion because it takes effective action to reduce the City’s structural deficit through significant expenditure reductions and targeted revenue increases.

November 3, 2010

The Civic Federation opposes the proposed FY2011 City of Chicago budget of nearly $6.2 billion because it does not effectively address the structural deficit and relies too heavily on asset lease reserve funds and debt restructuring to close the $654.8 million budget deficit. The proposed budget would defer costs and postpone changes needed to align current year expenditures with recurring revenues.

November 18, 2009

The Civic Federation opposes the FY2010 City of Chicago budget of $6.14 billion because it is unsustainable and relies too heavily on one-time reserve funds to close a $520.0 million budget deficit.

November 5, 2008

The Civic Federation supports the FY2009 City of Chicago budget of $5.97 billion because it does not rely on raising property tax and begins the painful yet necessary step of reducing payroll by 2,618 full-time equivalent positions to balance the budget.

October 31, 2007

The Civic Federation opposes the City of Chicago's proposed $5.9 billion budget. The budget proposes an additional $266.6 million in new spending and includes a $108.0 million property tax increase, the largest in recent Chicago history. We believe that the 15.1% property tax increase should be rejected and the city should maintain its self-imposed property tax cap.

November 1, 2006

The Civic Federation supports the City of Chicago's proposed $5.7 billion budget but has serious concerns about the poor health of the City's pension funds and the low level of reserve funds for contingencies.

November 30, 2005

The Civic Federation supported the City's holding the property tax levy constant for the third year in a row and eliminating vacancies, but was concerned by the lack of transparency regarding the funding for operations at Millennium Park, and by the use of borrowing to finance those operations.

December 1, 2004

The Civic Federation supported the City's holding the property tax levy constant for the second year in a row and cutting positions, but was concerned that further measures to control personnel expenditures should be taken and was disappointed that the City did not dedicate more Skyway sale revenues for long-term obligations.

November 5, 2003

The Civic Federation supported Chicago’s FY2004 budget of $4.8 billion because: 1) the City has made continued efforts to control personal services costs by reducing personnel over time; 2) The City’s net appropriation has increased an average of 2.6% per year over the last five years, on par with inflation; and 3) The City did not increase its property tax levy.

DOD audit acronym primer

November 6, 2018

In coming weeks the Department of Defense (DOD) will issue the results of a comprehensive financial statement audit. The effort has been described by Pentagon Comptroller David Norquist as “the largest ever undertaken.”

Defense Department accounting and financial reporting issues have been the principal reason the U.S. Government Accountability Office (GAO) has delivered a disclaimer (flunking) opinion on the consolidated financial statements of the federal government every year for the last two decades.

Trillions of dollars later, we may actually be making some progress in this area, though that is a matter of debate.

For anyone who wants to get up to speed on understanding the issues involved, one of the barriers to an informed debate and discussion is the bewildering array of acronyms and special terms attached to DOD audit issues.

As a small step toward trying to help inform that debate, following is a list of 45 acronyms used to describe various entities, concepts and laws relating to DOD accounting and auditing, together with links to descriptive websites.

For further background on the audit and the reasons why it matters, and remains worth monitoring, see “Auditing the Defense Department: A Primer,” a blog post I wrote back in May.

Best of luck on your mission.

AFR

CAP

CFOA

Chief Financial Officers Act of 1990

CIGIE

Council of the Inspectors General on Integrity and Efficiency

COP-OCO

Comprehensive Oversight Plan -- OCO

CRM

CRS

Congressional Research Service

DCAA

DFAS

Defense Finance and Accounting Services

DHA

DHP

DII

DISA

Defense Information Systems Agency

DLA

DMRDP

Defense Medical Research and Development Program

DOD OIG

Department of Defense Office of Inspector General

ERP

FASAB

Federal Accounting Standards Advisory Board

FCRA

Federal Credit Reform Act of 1990

FFRDC

Federally Funded Research and Development Centers

FIAR

Financial Improvement and Audit Readiness

FMFIA

Federal Managers Financial Integrity Act of 1982

GAGAS

Generally Accepted Government Auditing Standards

GAO

Government Accountability Office

GF

GFEBS

General Fund Enterprise Business Systems

GMRA

Government Management and Reform Act of 1994

IPA

Independent Public Accounting Firm

JFMIP

Joint Financial Management Improvement Program

MHS

MICP

Managers' Internal Control Program

OASDHA

Office of the Assistant Secretary of Defense for Health Affairs

OCO

Overseas Contingency Operations

OMB

Office of Management and Budget

PAR

Performance and Accountability Report

SFFAC

Statements of Federal Financial Accounting Concepts

SFFAS

Statements of Federal Financial Accounting Standards

SIGAR

Special Inspector General for Afghanistan Reconstruction

SRO

USACE

United States Corps of Engineers

USC

USDC

Undersecretary of Defense (Comptroller)

USSGL

USSOCOM

United States Special Operations Command

WCF

Cash is King! Wait a minute …

November 7, 2018

In 1913, on the heels of the then-worst financial crisis in U.S. history, Congress created the Federal Reserve. At the time, the Fed was conceived principally as a ‘lender of last resort,’ a source of liquidity (cash) in the event of widespread bank runs like those that erupted in the Panic of 1907.

Over time, the importance of this beast for the supply of money and credit, and, in turn, interest rates, became increasingly apparent. In the 1977 Federal Reserve Reform Act, Congress developed a directive for the Fed in conducting monetary policy that still exists today.

Section 2A of the Federal Reserve Act is a one-sentence section titled “Monetary Policy Objectives.” It reads:

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

So our Congress, in its infinite wisdom, has seen fit to direct 12 people to control the total amount of money and credit for more than 300 million people.

Faced with such a task, you have to try to count all that stuff up somehow. The Fed has developed accounting for money in its ‘monetary aggregates,’ which are also referred to as measures of the ‘money supply.’

Last week, Steve Hanke of Johns Hopkins University penned an article for Forbes titled “The Fed’s Misleading Money Supply Measures.” Hanke is a monetarist, someone who believes in the central importance of money as a driving force in economic growth and inflation. Hanke thinks money is important, and also thinks that the Fed doesn’t do a good job adding all that stuff up.

In his article, Hanke introduces the work of William Barnett, an economist who has led the development of alternative monetary statistics. In his 2012 book “Getting It Wrong,” Barnett tells the history of his work in this area as an economist at the Federal Reserve Board of Governors, as well as the story of his departure from the Fed.

Barnett makes a case that the Fed wrongly adds different things up at the same weight when accounting for money. The Fed’s narrow M1 aggregate basically includes cash circulating outside of banks as well as demand deposits in bank accounts. From there, the Fed produces (at least historically) progressively broader (and larger) aggregates of money. For example, M2 adds savings deposits and individual savings in money market mutual funds to M1. And the Fed used to report M3, which added other stuff (like institutional money market funds, Eurodollars, repos, and time deposits) to M2.

Barnett’s concern has been that the Fed has been accounting for all these different types of money at equal weights, when different types of money have different degrees of ‘moneyness.’ He has developed statistical measures adjusting different types of money at different weights, and believes they are a more valid representation. Hanke’s summary of his argument is that broader measures of money supply are important, but they should also discount the weight of progressively broader types of ‘money.’

I’m going to argue that this argument should matter, fundamentally, for ‘narrow’ measures of money as well – and in the line item at the top of the balance sheet for companies as well as state and local governments. That line-item is called “Cash and cash equivalents.”

Cash includes two main things – currency circulating outside of banks, and deposits in banks.

And speaking of adding up unequal things at equal weights, consider what people thought of these two things at the time of the Panic of 1907. Did they think they were equal? Far from it. People were panicking! They wanted the good stuff, not the bad stuff.

From there, generally accepted accounting principles enshrined a fundamental falsehood at the top of the balance sheet, inviting decades of government subsidies, interventions, regulations, and bailouts designed (in principle) to try to make these unequal things equal. In turn, these interventions generated moral hazard driving our latest and greatest financial crisis, and continued risk in our financial system today.

Question: If “cash” is not equal to itself, how can “cash equivalents” even exist?

“Cash is King!” they say. Perhaps Cash really is king-like, given that arbitrary tyrannical authority ends up determining if it is really cash or not.

More to follow …

You think you don't own any stocks? Think again

November 12, 2018

The National Public Pension Coalition (NPPC) represents public-sector employees and their interests in retirement benefit plans. On the “About Us” page at its website, the organization states that “NPPC believes every American should be able to retire in dignity. … The NPPC is working to preserve the financial security of all workers for generations to come.”

The NPPC also states that “We also know that there is no one more interested in strengthening the public pension system than the public employees who are counting on pensions to retire.”

Today, Pensions & Investments had a story by Brian Croce headlined “Voters reject candidates in 3 states who lobbied for switch to DC plans.” The article quoted Bridget Early, executive director of the NPCC, “Even when there were attempts to vilify public employees and defined benefit plans and suggestions that everyone should have 401(k)s, I think folks are starting to understand that (retirement security) is very important to the economy.”

Right now, at 1:40pm CT, the Dow is down more than 400 points. Most pension plans are dominated by riskier investments like stocks, real estate, and private equity. Are public pension plan participants concerned?

Maybe not as much as taxpayers or voters are, or should be.

Defined benefit plans offer defined benefits. That’s what makes them safer, on the surface, than 401(k) plans – at least for the people in the plan, especially in public plans in states (like Illinois) where benefits are not only defined but protected by law.

Does that mean these plans aren’t risky? Not for citizens and taxpayers responsible for funding those plans. For those folks, these plans are very risky as they have to make up for any downside.

Retirement security for me, but not for thee.

Should ‘future generations’ care about U.S. government financial trends?

November 14, 2018

Future generations, by definition, don’t exist yet. But ...

If future generations could care about U.S. government finances, would they?

Let’s ask that question the other way around. Should the U.S. government care about future generations?

Whether or not the U.S. government should care, does the US government care about future generations?

Reading the financial report of the federal government, there are some simple cues that the government is at least giving lip service to the idea.

When faced with massive, complex financial statements, either for publicly traded companies or for governments, there are times when simple cues can help inform analysis.

The chart below shows the number of times the term ‘future generations’ is used in the annual financial report of the US government, from 2005 to 2015:

In turn, here’s a chart showing the number of times the word “sustain” appears, either in the term “sustainable,” “unsustainable,” or “sustainability.” These references arise most frequently in discussions on whether and for how long US government finances are sustainable, in light of the implied massive future increases in debt and interest expense under current law, policy, and demographic expectations.

The references to ‘future generations’ and ‘sustain’ have both risen ten-fold since 2005, either because the government really cares more than it used to, or because it thinks it is more important to give lip service to the issues.

Either way, however, this is a bit of a red flag. Anyone who cares about young people, or future generations, or their own future after-tax, after-inflation wealth, should be paying attention to the public purse.

DOD audit report slated to be released today

November 14, 2018

Today, the U.S. Department of Defense will release the results of what has been called the “first-ever department-wide financial audit.”

The Defense Department’s financial statements are actually audited every year. And the failure of the DOD to secure clean, “unmodified” audit opinions have been the principal reason why the Government Accountability Office has delivered a disclaimer of opinion on the overall financial statements of the U.S. Government – every year since the late 1990s.

The new DOD audit initiative does represent a first, however, in how comprehensive it was. The audit will likely provide some valuable new insights and opportunities in improving the trustworthiness of DOD financials.

There will likely be massive media coverage of the release of the report. Looking ahead, here are some questions to consider:

· Which individuals stood out for their leadership and results in improving accounting controls and processes before the audit got underway?

· Who stands out for their performance during the audit, and in applying lessons learned for the future?

· Were any members of Congress helpful in providing feedback and/or valuable oversight during the audit initiative?

· Who have been some of the better reporters covering the issues involved? Either in the mainstream or alternative media? Have any of their insights been especially valuable in the overall effort?

· Which of the independent public accounting firms associated with the audit provided the most valuable service? Did any of them fail to measure up?

· How should the public try to gauge the cost-effectiveness of the money spent on this audit?

· Recent financial market history may provide some valuable perspective. Have you seen the movie “The Big Short?” Have you read the book “The Smartest Guys in the Room?” Have you reflected on the costs and benefits of paying ‘independent’ auditors for their opinions?

· Can or should we measure the success of the audit initiative on the basis of how many scandals were uncovered?

· Can blockchain technology help to address identified weaknesses? What progress is DoD making in this area? Do you see any shortfalls or risks in new accounting technologies for the integrity of the financial reporting process?

· What do these results imply about the cost-effectiveness of the quality of ‘national defense?’ Is there a way to identify what % of current spending levels could achieve equivalent ‘defense,’ holding foreign policy (and the international footprint of ‘national defense’) constant?

· If DoD financial accounts may be ‘modified’ to guard secret classified programs, will DoD ever receive anything but a disclaimer of opinion on its financial statements?

· After reflecting on the audit process, what are some of the strengths and weaknesses of federal government accounting standards? Where could they be improved?

Illinois teachers -- help wanted now

November 20, 2018

I just saw something interesting, and potentially disturbing, on the Illinois Teachers' Retirement System website.

The front page still has a notice that reads:

“A new law addressing Illinois’ teacher shortage problem takes effect with the 2018-2019 school year. Retired TRS members can teach 120 days or 600 hours without affecting their pensions. This change is in effect through the 2019-20 school year.”

In theory, pensions are for retired people, not people earning money while working. Is that how this law works?

Is the 120-day or 600-hour restriction cumulative? Or can teachers teach for 120 days, take some time off, and then start teaching again?

More importantly, what about this “teacher shortage problem?”

Pension funds are financial institutions, like banks and insurance companies. They take money in the door, and put it to work.

Pension funds and insurance companies are a little bit different than banks in one key way: banks can be subject to “run on the bank” issues. If counterparties lose confidence in banks, and withdraw large sums of money, other counterparties may join the party, worried that if they don’t, they will be at the end of the line when nothing is left.

Pensions and insurance companies, however, can be subject to different types of “death spirals” if new money stops coming in the door.

What is happening to the ability to inspire young people to pursue careers as teachers, firefighters and cops in states like Illinois, Connecticut, New Jersey and Kentucky—to name a few—where public pension funds are in very bad shape?

In turn, what is happening to the ability of the pension funds for those employees to depend on future contributions from new and future participants?

Happy Thanksgiving!

Charlotte—an exception to a rule

November 27, 2018

Do finance-heavy cities have governments with relatively strong finances? How about their states?

Consider New York City, Chicago, Hartford, and Charlotte.

New York City, home of the Big Banks and Wall Street. Chicago, with LaSalle Street, banks, insurance companies, and futures and options markets. Hartford, the “insurance capital of the world.”

And Charlotte, now considered the second-largest banking center in the nation.

One might instinctively think that governments in cities with a lot of financial talent and tradition could or should be doing relatively well, themselves, financially.

But that is far from the case.

Truth in Accounting’s analysis of the financial condition of the 75 largest cities ranked Chicago and New York City second-to-last and last, respectively, in terms of their municipal governments’ financial condition. Charlotte ranked No. 4.

While Hartford’s population doesn’t qualify for our annual city report, here’s a look at a related metric (unrestricted net position per capita) in 2010 and the latest fiscal year for New York City, Chicago, Hartford—and for Charlotte.

Reported unrestricted net positions deteriorated significantly, on a per capita basis, for New York City, Chicago, and Hartford, from 2010 to 2017, with significant negative holes in this measure (roughly comparable to shareholder equity, or assets less liabilities, in the private sector).

In government accounting, unrestricted net position helps assess how effectively a jurisdiction has shepherded resources responsibly, avoiding spending beyond current revenues in ways that shift costs to future taxpayers.

On that score, Charlotte is a splendid and shining success, compared to other major financial centers.

And we tend to see the same pattern for the states that are home to these cities.

The chart below shows Truth in Accounting’s rankings for the financial conditions of Connecticut, Delaware, Illinois, New Jersey, New York, and North Carolina. All of these states rank in the bottom 10 of the 50 states—except for North Carolina, which ranks about average among the 50 states.

What is going on here? Why are financially intensive city-states in relatively worse financial shape? What lessons can Charlotte provide?

Page ix (pdf page 13) of Charlotte's latest Strategic Operating Plan, titled "Finance and Budget Principles," could be a good place to start.

How much does FRED cost?

December 5, 2018

Jeffrey Tucker recently wrote an article for the American Institute for Economic Research that examines the costs and benefits of eliminating the Federal Reserve. Tucker contends that the dislocation and transition costs associated with ditching a central bank aren’t as high as one might think. Looking at the services and benefits the Fed assertably provides, Tucker took note of how market forces could deliver those services as well—and perhaps even better—in light of the historical record of the Fed and financial stability.

Among the benefits provided by the Fed, Tucker points out one very interesting service that wouldn’t necessarily go away if the Fed didn’t exist. FRED is an excellent, reliable, massive and consistently updated database of economic, financial and other information that resides on the website of the Federal Reserve Bank of St. Louis. It’s a remarkable resource that’s used by many people in financial markets, the media, and the blogosphere. It is also “free.”

Would FRED disappear if the Fed were eliminated?

In his article, Tucker writes “It’s true that the St. Louis Fed has the best online tool for data reporting but how many people know that this is actually outsourced to a private sector firm?”

If the St. Louis Fed outsources FRED, how much does it pay the vendor(s)?

Consider the market for databases, a market little old Truth in Accounting competes in with our State Data Lab resource. What if we are competing with a wonderful, massive and reliable system such as FRED, which is paid for by an organization that prints money?

If FRED is outsourced, that would help explain why, a couple years ago, when I asked folks at the Federal Reserve Bank of St. Louis how many people were working on this wonderful resource, I was told "That depends on who you ask."